Lesson 4.1: Cash Flow Management

The Profit Illusion

Many South African entrepreneurs confuse sales with cash. You might have R100,000 in outstanding invoices (profit on paper), but only R5,000 in your bank account. This is the cash flow trap that kills 60% of small businesses within their first three years.

Real Example

Sipho’s electrical contracting business wins a R500,000 government tender. On paper, his profit margin is 25% (R125,000 profit). However:

– Materials cost R300,000 (paid upfront to suppliers)

– Labour costs R75,000 (paid weekly)

– Government payment: 90 days after completion

– Result: Despite being “profitable,” Sipho runs out of cash and can’t pay his team

The Cash Flow Survival Framework

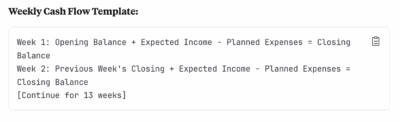

1. The 13-Week Rolling Forecast

Create a weekly cash flow forecast that looks 13 weeks ahead. This gives you enough runway to spot problems and take action.

2. The Cash Conversion Cycle

Understand how long it takes to convert your investment into cash:

Formula: Days to collect payment + Days inventory sits – Days you can delay supplier payments

Example for a small retailer:

– Buy inventory: Day 0 (cash out)

– Sell inventory: Day 45 (still no cash in)

– Customer pays: Day 75 (cash finally comes in)

– Cash conversion cycle: 75 days of cash tied up

3. Early Warning Signs of Cash Flow Problems

Red Flags to Watch:

– Taking longer to pay suppliers

– Increasing reliance on overdraft facilities

– Customers asking for extended payment terms

– Inventory levels growing faster than sales

– Personal funds being used for business expenses

– Staff asking about delayed salaries